The Dow Jones Industrial Average plunged through the psychologically important 16,000 mark in yesterday’s sell-off, while the S&P 500 and Nasdaq slid 2% and 2.3%, respectively.

But in Japan, a Lunar New Year’s treat for investors: The ever-volatile Nikkei 225 snapped a four-day losing streak to end up 1%. That’s performance that most American investors would kill for right now.

For that, we can look to Bank of Japan chief Haruhiko Kuroda, a faithful practitioner of the “Abenomics” that have kept Japan’s stock markets curiously (some may say insanely) buoyant in these sell-happy times… only at the cost of wrecking the country’s long-term economic health.

Kuroda created shockwaves late last month when he announced he was taking a key Japanese deposit rate negative, bringing the worldwide total of sovereign debt “paying” negative interest to $5 trillion.

I don’t doubt that Yellen & Co. are watching events in Japan’s central banking sector and stock market with equal parts anxiety and interest: They have a foundering economy and a plunging stock market on their hands – even if they’re not “officially” supposed to care about the stock market.

Those markets have reached a state of “bad news is good news” again, with markets rallying a bit as they price in a more dovish stance behind disappointing economic data.

That’s cutting off the Fed’s options, and soon the only logical place for the Fed to turn will be more easing… and negative deposit rates.

So today I’m going to show you the investment to own for the liquidity crisis that’s bound to follow – and ruin the unprepared…

The Bank of Japan Is Desperate

That’s why, in a surprise move, it just introduced a deposit rate of -0.1% for commercial banks. What that means is banks will now have to pay rather than be paid for hoarding cash.

The goal is to get banks to loosen their grip on cash and start lending it, in an effort to stimulate economic activity.

It’s an uphill battle, as spending has remained sparse despite near-zero rates for some time already.

But it’s also a sign of desperation, as the Bank of Japan recently announced it was delaying its outlook for achieving its targeted 2% inflation by at least six months. That’s already the second time since October 2015.

And this after forcing trillions of yen into the Japanese financial system. OK, so stocks doubled in the process, but the economy has endured no less than three recessions since 2010.

Incredibly, Japan had a cautionary example for its negative-interest-rate project (NIRP): Europe. The policy has been a disaster there, too.

It’s going to take these countries a long time to dig out from under these experiments…

Europe: The First of the Worst

The European Central Bank (ECB) was the first major central bank to institute sub-zero deposit rates – a year and a half ago.

But that wasn’t enough. On Dec. 3, 2015, the ECB lowered rates further to -0.3% on overnight deposits.

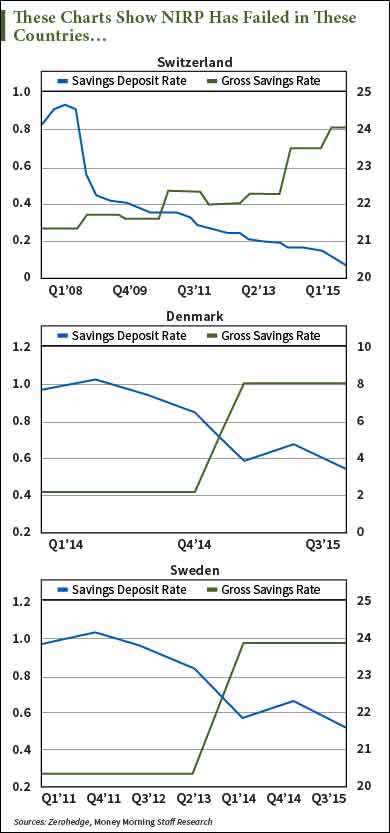

And the ECB’s got company, with other European economies outside the Union. Sweden’s key rate is running at -0.35%, Denmark’s is down at -0.75%, and Switzerland takes the top spot at -1.1%.

Considering that the goal is to get people to borrow and spend more, this unusual policy has clearly failed. Have a look at how this half-baked tactic has worked out for these three nations.

In words, these charts are telling us that, as bank interest rates have approached zero, people have instead increased their savings.

That’s clearly failed mission for those central banks.

But clear and utter failure is no reason the Fed’s own geniuses won’t pull the very same futile stunt.

Bernanke Returns to Suggest NIRP for United States

You don’t have to listen all that hard to hear the ever louder and increasingly frequent warnings that NIRP is headed for the United States. The evidence is becoming more compelling by the day.

Fourth-quarter GDP data recent revealed economic growth of 0.7% between October and December; a pale shadow of the 2% rate that was reported for Q3.

Even the Fed couldn’t sweep reality under the rug, acknowledging that “economic growth slowed late last year.” The U.S. Department of Commerce noted that Q4 real gross domestic demand was cut in half to 1.1% versus Q3’s 2.2%.

Like in Europe, the American people are just not spending.

James Grant, editor of Grant’s Interest Rate Observer, recently told Bloomberg TV Canada, “The Fed is going to recant and reverse… There’s an important chance it will return to zero or some policy equivalent to zero, some new outbreak of stimulus.”

Grant believes the United States is already in a recession.

Former Fed Chair Ben Bernanke told MarketWatch that he believes the Fed should consider using negative rates to fight the next serious economic slowdown. Emphasis mine.

I guess “Helicopter” Ben doesn’t have access to the same data we do, like the three simple charts I just showed you.

But perhaps most intriguing are the trial balloons being floated by the Fed.

The most recent one, following on previous hints by New York Fed President Dudley and former Minneapolis Fed President Kocherlakota, comes from no less than current Fed Vice Chair Stanley Fischer.

Fischer just said in a Bloomberg interview that NIRP was working “more than I expected.”

I’m not sure just what indicator Fischer has used to reach his conclusion, but then again the Fed’s never let real data get in the way of a bad decision.

Now the Fed will stress test big banks under a scenario where three-month treasury yields go negative in Q2 2016 then drop to -0.5% and stay there until early 2019.

Folks, it’s time to prepare for the United States to be NIRP’ed.

The Best Investment to Beat NIRP

The world is headed down a path of exploding debt, fiat money, and negative interest rates for which there’s simply no historical precedent.

In this scenario, your best line of defense is to own some gold and silver as both insurance and for the serious upside potential.

I know this may sound simplistic. But it appears that advice has yet to be heeded by the vast majority of Americans.

While reliable data on gold ownership in the United States is admittedly hard to come by, the best estimates point to numbers in the low single digits. Some experts place it below 3%.

My top recommendation is to acquire to real, hold-in-your-hand gold and silver coins and/or bars.

But I know many simply want to own gold and silver in the easiest way possible. Enter exchange-traded funds (ETFs).

If you’re going to go that route, then consider these.

A top choice among gold ETFs is the Sprott Physical Gold Trust (NYSE Arca: PHYS). It holds gold bullion that is fully allocated and stored at a secure third-party location in Canada, subject to periodic inspections and audits.

There is no levered financial institution between investors and the gold, plus U.S. investors holding for at least 12 months can benefit from a 15% (approximately) capital gains tax versus the 28% rate with most precious metals ETFs.

For silver, have a look at the Sprott Physical Silver Trust ETF (NYSE Arca: PSLV). PSLV also holds its silver bullion fully allocated and stored, as is the gold held in PHYS, and it’s subject to the same periodic inspections and audits.

Here too there’s no levered financial institution involved, and the tax advantages for U.S. investors are similar to PHYS.

Just remember, if you wait to buy this form of insurance when everyone else realizes its true value, odds are it’s going to cost you a whole lot more.

Follow Money Morning on Facebook and Twitter.

About Money Morning: Money Morning gives you access to a team of ten market experts with more than 250 years of combined investing experience – for free. Our experts – who have appeared on FOXBusiness, CNBC, NPR, and BloombergTV – deliver daily investing tips and stock picks, provide analysis with actions to take, and answer your biggest market questions. Our goal is to help our millions of e-newsletter subscribers and Moneymorning.com visitors become smarter, more confident investors.To get full access to all Money Morning content, click here.

Disclaimer: © 2016 Money Morning and Money Map Press. All Rights Reserved. Protected by copyright of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including the world wide web), of content from this webpage, in whole or in part, is strictly prohibited without the express written permission of Money Morning. 16 W. Madison St. Baltimore, MD, 21201.